BIX ARTICLE

Investing in Banks' Capital Bonds and Sukuk

Jan 16, 2020

|

7 min read

Featured Posts

Social Bonds Illustrative Use-Of-Proceeds Case Studies Coronavirus

Jul 06, 2020

|

2 min read

Sustainable Banking Network (SBN) Creating Green Bond Markets

Jul 06, 2020

|

2 min read

Why is Inflation Making a Big Comeback After Being Absent for Decades in the U.S.?

Mar 24, 2022

|

7 min read

SC issues Corporate Governance Strategic Priorities 2021-2023

Mar 29, 2022

|

3 min read

Why Invest in Banks’ Capital Bonds and Sukuk?

Introduction

| How the bank fund their operations?

The bank usually use our deposits (see term deposits) for lending – that’s how the Loan-to-Deposit (LDR ratio) can be a very useful tool to gauge how much of our money is used by the bank as loans. As of September 2019, Malaysia’s banking system LDR is reportedly at 88.5%, which means RM0.885 was lent out by the banks for every RM1.00 of our deposit, which is healthy compared to certain countries with more than 100% LDR.

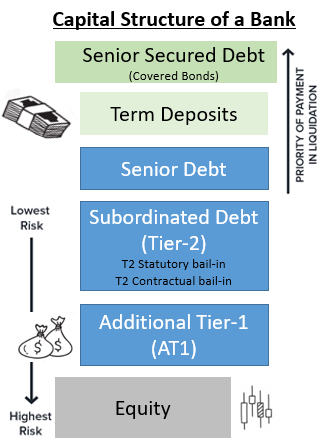

Besides deposits, banks can borrow from the capital markets in three usual structure – 1) senior debt; 2) subordinated debt (a.k.a Tier-2 capital) and 3) additional tier-1 capital (a.k.a AT1).

|

.png "Capital Structure of The Bank") |

Five reasons to invest in Banks’ Capital Bonds/Sukuk

#1 – All Malaysian banks are Investment-Grade at every layer of capital

| Rating | Top-6 | Mid-Small | Foreign-backed |

| AAA | MBB, CIMB, PBB, HLBB | OCBC, UOB, HSBC, SCB | |

| AA1 | MBB, CIMB, PBB, HLBB (Tier-2) | OCBC, UOB, HSBC (Tier-2) | |

| AA2 | RHB, AMBB | OCBC AT1 | |

| AA3 | PBB AT1 RHB, AMBB (Tier-2) |

AFFIN, BIMB | CIMB THAI |

| A1 | CIMBGH AT1 HLBB, RHB, AMBB AT1 |

ALLIANCE, AFFIN, BIMB (Tier-2) | |

| A2 | ALLIANCE Tier-2 MBSB |

||

| A3 | MBSB Tier-2 AFFIN AT1 |

||

| BBB1 | ALLIANCE AT1 | ||

| BBB2 | MBSB AT1 | ||

| BBB3 |

#3 More Shariah-compliant financial instruments on offer compared to stocks

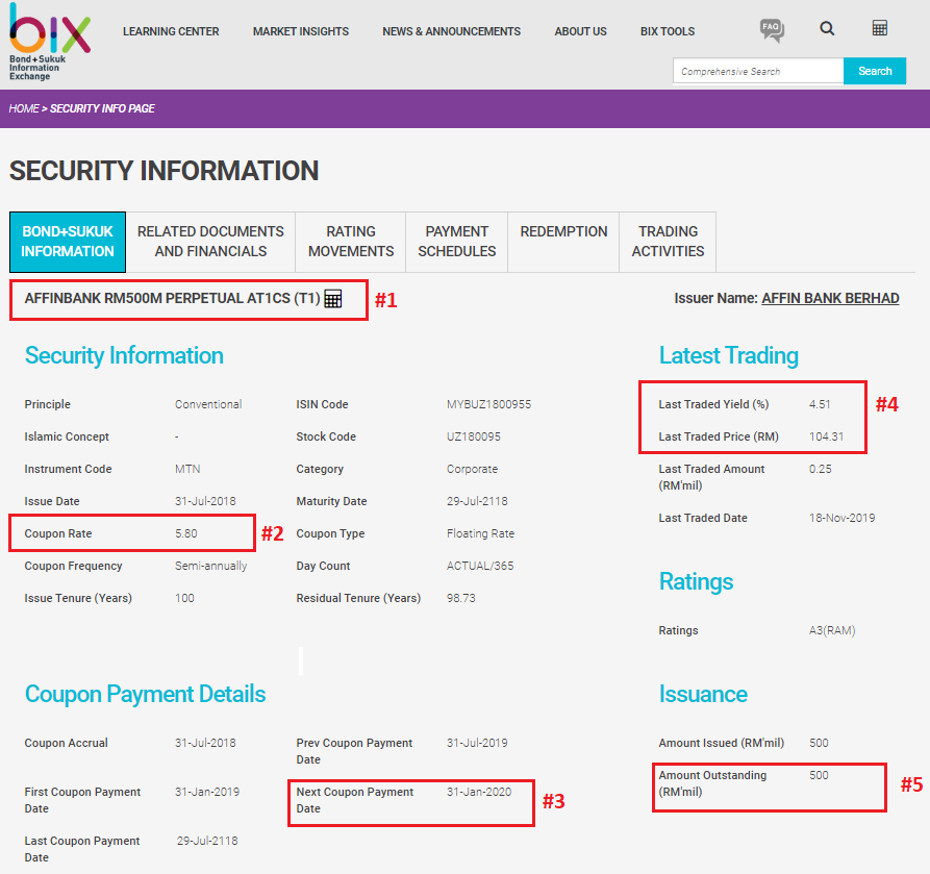

#4 There are values across the capital structure of the bank you like

The table illustrates how we can plot potential yield at different level of capital

https://www.bixmalaysia.com/Security-Info-Page.aspx?SBID=6636

.png "Banking Capital Bonds and Sukuk")

Author profile

Fakrizzaki Ghazali was a Fixed Income portfolio manager and analyst in an

investment management firm in KSA, covering GCC and Global Sukuk markets. He previously worked as a credit strategist at one of Malaysia’s sell-side research house; also used to serve a private bank in Kuala Lumpur with focus on generating bottom-up ideas from both Investment Grade and High Yield bonds in the Asian credits space. Fakrizzaki started as an analyst at a local asset management having debuted his career as an auditor in one of the Big-4 firm. The article is his own opinion from experience in the industry for over sixteen years. He believes that retail investors need more high-yield ideas and be constantly guided as there are sufficient low-risk, high-quality bonds/sukuk offered in the market.

investment management firm in KSA, covering GCC and Global Sukuk markets. He previously worked as a credit strategist at one of Malaysia’s sell-side research house; also used to serve a private bank in Kuala Lumpur with focus on generating bottom-up ideas from both Investment Grade and High Yield bonds in the Asian credits space. Fakrizzaki started as an analyst at a local asset management having debuted his career as an auditor in one of the Big-4 firm. The article is his own opinion from experience in the industry for over sixteen years. He believes that retail investors need more high-yield ideas and be constantly guided as there are sufficient low-risk, high-quality bonds/sukuk offered in the market.Disclaimer

This report has been prepared and issued by Bond and Sukuk Information Platform Sdn Bhd (“the Company”). The information provided in this report is of a general nature and has been prepared for information purposes only. It is not intended to constitute research or as advice for any investor. The information in this report is not and should not be construed or considered as an offer, recommendation or solicitation for investments. Investors are advised to make their own independent evaluation of the information contained in this report, consider their own individual investment objectives, financial situation and particular needs and should seek appropriate personalised financial advice from a qualified professional to suit individual circumstances and risk profile.

The information contained in this report is prepared from data believed to be correct and reliable at the time of issuance of this report. While every effort is made to ensure the information is up-to-date and correct, the Company does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information contained in this report and accordingly, neither the Company nor any of its affiliates nor its related persons shall not be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

YOU MAY ALSO LIKE

ARTICLE

Jun 04, 2026

|

4 min read

ARTICLE

May 11, 2026

|

6 min read

ARTICLE

May 04, 2026

|

4 min read

ARTICLE

Mar 02, 2026

|

4 min read