BIX ARTICLE

What Is Green Bond & Sukuk?

May 16, 2018

|

4 min read

Featured Posts

Social Bonds Illustrative Use-Of-Proceeds Case Studies Coronavirus

Jul 06, 2020

|

2 min read

Sustainable Banking Network (SBN) Creating Green Bond Markets

Jul 06, 2020

|

2 min read

Why is Inflation Making a Big Comeback After Being Absent for Decades in the U.S.?

Mar 24, 2022

|

7 min read

SC issues Corporate Governance Strategic Priorities 2021-2023

Mar 29, 2022

|

3 min read

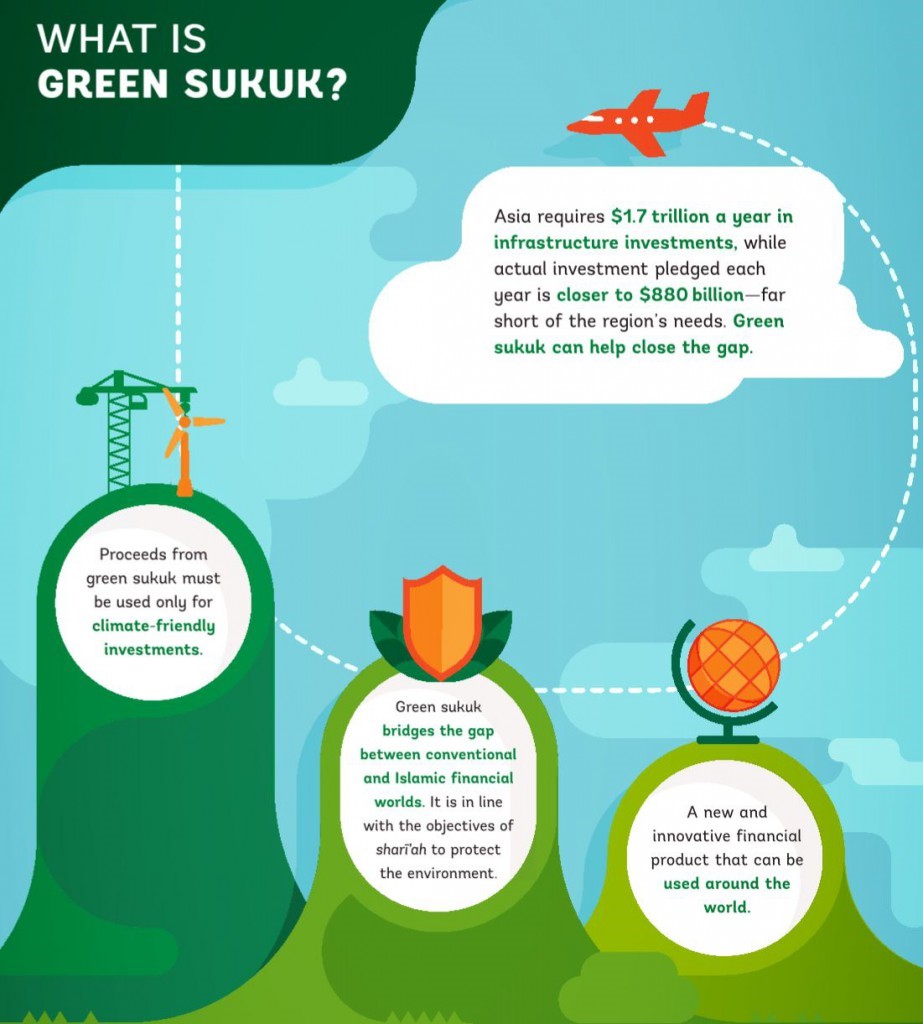

Since most investors in environment sustainability want to know precisely how their money will be used, bonds that are general obligations of an issuer have limited appeal unless all activities of the issuer meet the investor’s environmental standards. Sukuk, which are most like a conventional fixed-income security, could help fill the fixed income supply gap for environmental investors, to the extent the proceeds of a sukuk are earmarked for an environmentally-beneficial purpose.

The growing trend toward green bond and sukuk is mainly due to the natural progression of fixed income market, the growing awareness of investors toward ethically and socially responsible investment and the stricter capital requirements for the bank to finance infrastructural projects.

One of the areas that are normally associated with SRI is the environment and its preservation. Green bond therefore becomes a common instrument to serve this aspect of SRI in the global market. For example, in 2007 the European Investment Bank (EIB) launched a EUR 600mln climate awareness bond focusing on renewable energy and energy efficiency.

Subsequently in 2008, World Bank issued a total of USD440mln green bond to support climate-focused program for the Scandinavian pension. In 2013, the African Development Bank issued a USD500mln green bond to finance climate change solution in Africa. As of June 2015, the World Bank has issued over 100 green bond papers valued at USD8.5bln.

In Malaysia, Tadau Energy Sdn Bhd, a Malaysian-based renewable energy and sustainable technology investment firm issued SRI sukuk on the Syariah principles of istisna’ (manufacturing sale) and ijarah (leasing) in July 2017. The RM250 million Green SRI Sukuk Tadau is to finance the construction of large scale solar (LSS) photovoltaic power plants in Kudat, Sabah, with a tenure of two to 16 years.

Following the success of SRI Sukuk Tadau, Quantum Solar Park Malaysia Sdn Bhd launched the world’s largest green SRI sukuk of RM1 billion in October 2017 to fund the construction of Southeast Asia’s largest solar photovoltaic plant project in three districts: Kedah, Melaka and Terengganu.

Securities Commission Malaysia (SC) launch the issuance of Malaysia’s first green sukuk in July 2017 which is an innovative channel to address global funding gaps in green financing under its Sustainable & Responsible Investment (SRI) Sukuk framework. To complement SRI Sukuk framework and promote greater utilisation of green sukuk as a fundraising channel, several incentives are in place to attract green issuers including:

- Tax deduction until year of assessment (YA) 2020 on issuance costs of SRI sukuk approved or authorised by or lodged with the SC;

- Tax incentives for green technology activities in energy, transportation, building, waste management and supporting services activities [www.mida.gov.my and www.myhijau.my]; and

- Financing incentives under the Green Technology Financing Scheme (GTFS) with total funds allocation of RM5 billion until 2022 [www.gtfs.my].

Download ASEAN Green Bond Standards report for additional reading

Download Report

Disclaimer

This report has been prepared and issued by Bond and Sukuk Information Platform Sdn Bhd (“the Company”). The information provided in this report is of a general nature and has been prepared for information purposes only. It is not intended to constitute research or as advice for any investor. The information in this report is not and should not be construed or considered as an offer, recommendation or solicitation for investments. Investors are advised to make their own independent evaluation of the information contained in this report, consider their own individual investment objectives, financial situation and particular needs and should seek appropriate personalised financial advice from a qualified professional to suit individual circumstances and risk profile.

The information contained in this report is prepared from data believed to be correct and reliable at the time of issuance of this report. While every effort is made to ensure the information is up-to-date and correct, the Company does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information contained in this report and accordingly, neither the Company nor any of its affiliates nor its related persons shall not be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

YOU MAY ALSO LIKE

ARTICLE

Aug 03, 2026

|

4 min read

ARTICLE

Jul 29, 2026

|

4 min read

ARTICLE

Jul 22, 2026

|

11 min read

ARTICLE

Jul 21, 2026

|

6 min read